The Tish James Indictment Looks Like Country Fried BS

Yeah, don't faint.

Last week Lindsey Halligan, the acting/interim/special/imaginary US Attorney for the Eastern District of Virginia indicted New York Attorney General Letitia James for mortgage fraud, fulfilling a long-held goal of her client, Donald Trump.

James is charged with two felonies relating to the purchase of an investment property in Norfolk: one count of bank fraud in violation of 18 U.S.C. § 1344, and one count of making a false statement on a mortgage application in violation of 18 U.S.C. § 1014.

As with the recent indictment of James Comey, another Trump nemesis, the James indictment was so weak that regular prosecutors — i.e. ones who have actually tried criminal cases — refused to touch it. And, as in Comey’s case, Halligan was the only lawyer willing to sign off on it. So if conservative commentators and Sam Alito(!) are right, and her appointment was unlawful, the case may get dismissed long before trial.

Meet Virginia

Prior to this indictment, it was presumed that Halligan would indict James with respect to a different Virginia property. Bill Pulte, head of the Federal Housing Finance Agency, as well as Fannie Mae and Freddie Mac, has been spelunking through financial records of Trump’s enemies, and he sent a criminal referral to Attorney General James regarding a house in Norfolk. But apparently Halligan punted on The Case of the Errant Power of Attorney, an extraneous document which erroneously described the property as a personal residence, when every other piece of the loan application correctly described it as a rental. Worst Nancy Drew mystery ever!

Instead she charged James with lying on a mortgage application for a different house in Norfolk, which James purchased in August of 2020 for $137,000. She received a loan for 80 percent of the purchase price from Old Virginia Mortgage (now known as OVM Financial), which she appears to have paid off in 2024.

According to the indictment, James falsely claimed that she planned to use the house as a second home in order to lower her interest rate from 3.815 to 3.0 percent, saving herself $17,837 over the four-year life of the loan. In a conclusory fashion, but without providing any evidence, it states that James “knowingly” made false statements on the loan document. This has a certain irony, since James prosecuted Trump for falsely inflating his net worth on mortgage applications, something he claimed was a victimless crime so long as the lender was paid in full. The government also claims that the reduced rate netted James just over an extra $1,000 in the seller’s credit at settlement.

The problem is that the indictment yaddayaddayaddas over several elements of the supposed crime, which strongly suggests that it was done on purpose because filling in the blanks would fatally undermine the prosecution.

The Low Rider

Paragraph 6 of the indictment alleges that:

The loan was originated by OVM Financial under a signed Second Home Rider, which required James, as the sole borrower, to occupy and use the property as her secondary residence and prohibited its use as a timesharing or other shared ownership agreement or agreement that requires her to rent the property or give any person any control over the occupancy or use of the property.

That language roughly mirrors Fannie Mae Form 3890, which James almost certainly signed as part of her mortgage application. It says:

6. Occupancy. Borrower must occupy and use the Property as Borrower’s second home. Borrower will maintain exclusive control over the occupancy of the Property, including short-term rentals, and will not subject the Property to any timesharing or other shared ownership arrangement or to any rental pool or agreement that requires Borrower either to rent the Property or give a management firm or any other person or entity any control over the occupancy or use of the Property. Borrower will keep the Property available primarily as a residence for Borrower’s personal use and enjoyment for at least one year after the date of this Security Instrument, unless Lender otherwise agrees in writing, which consent will not be unreasonably withheld, or unless extenuating circumstances exist that are beyond Borrower’s control.

Plainly the intent of that rider is that the borrower agrees to “maintain exclusive control” over the property. So, while James couldn’t turn the home into a time-share or sign an agreement that required her to rent the property, there was no bar to renting it in the short term. That’s why the rider says that James agreed to keep the property “available primarily as a residence.”

In fact, Fannie Mae revised this rider in 2019 to make it clear that buyers were free to rent out their second homes on sites like Airbnb. As one mortgage specialist noted at the time, the new rider “explicitly” allows for those sorts of short-term rentals of second homes. And so, even if James had rented out the Norfolk property, she probably wouldn’t have violated the Fannie Mae rider.

But Did James Even Rent Out Her Second Home?

The short answer is: We don’t know.

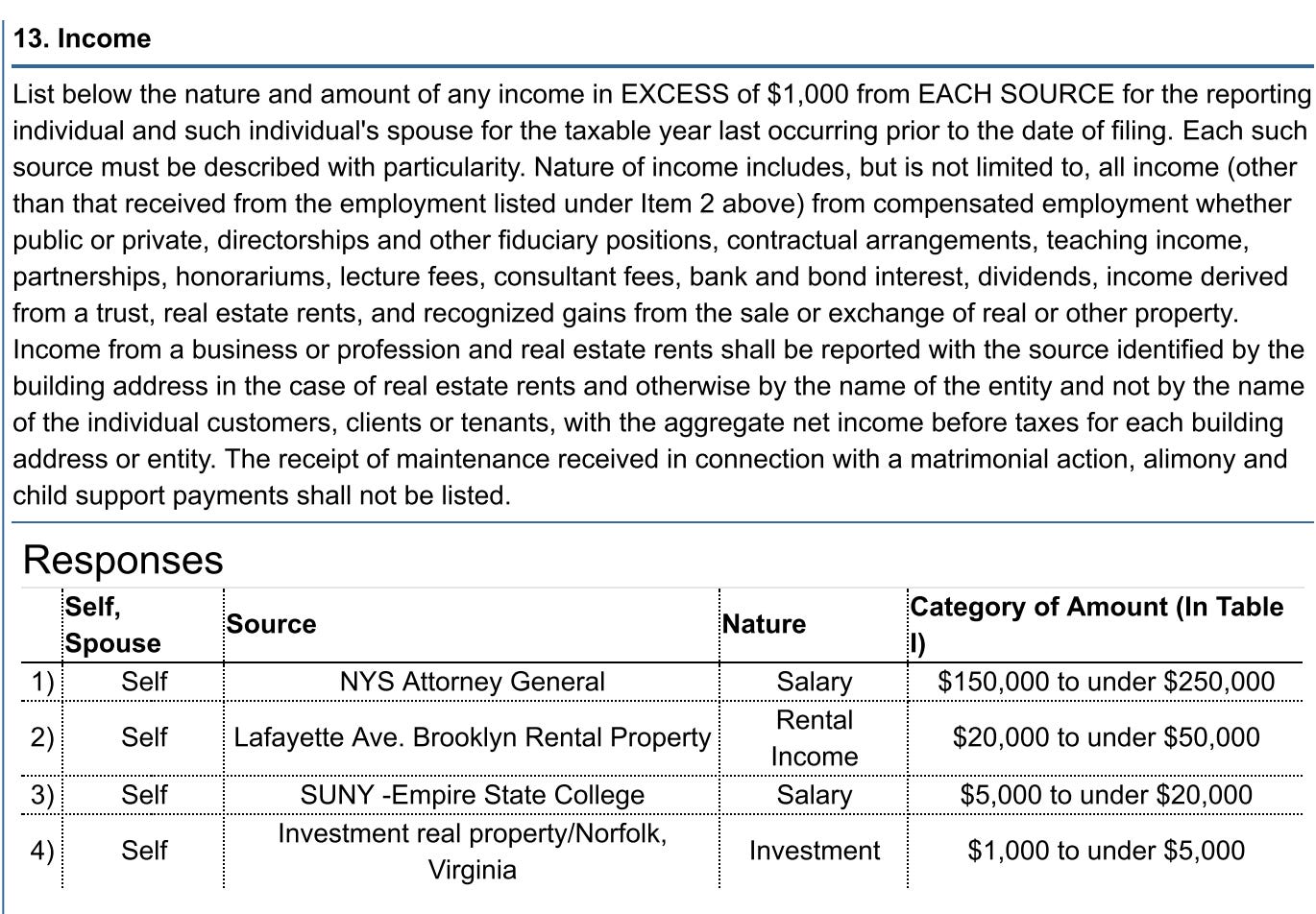

The indictment says that James rented the property to a family of three and collected “thousand(s) of dollars in rents received.” That seems deliberately vague, suggesting perhaps that James netted tens or even hundreds of thousands of dollars.

In fact, she netted somewhere between $1,000 and $5,000, according to a 2020 financial disclosure dug up by a “forensic accountant” named Sam Antar. In 2023, Antar was convicted of securities fraud in connection with the Crazy Eddie electronics chain, of which he was CFO. He’s since rebranded himself as an “investigator of financial fraud,” presumably on the theory of it takes one to know one. (Yes that) Roger Stone’s “Stone Zone” recently ran an exposé on James drafted by Antar which included such trenchant observations as:

Adding to the mystery, James consistently reported this mortgage in the range of $100,000-$150,000 for three consecutive years (2020–2022), but then in 2023, the reported value inexplicably drops to $75,000-$100,000 without explanation. While this could potentially be related to payment of principal, the absence of any official record of this mortgage in ACRIS [New York’s real property registration site] makes it impossible to verify the actual terms, origination date, or even existence of this substantial financial obligation.

She paid down her mortgage? Lock her up!

Here’s Antar’s smoking gun:

Note that James discloses “rental income” for a property in Brooklyn, but describes income on the Norfolk property as “investment.” According to the indictment, James rented the property to a family of three. But Halligan never says for how long, and she’s pretty hand-wavey about how much rent James took in — two things she almost certainly knows, since her predecessor Erik Siebert interviewed multiple witnesses about this case. Income of less than $5,000 is consistent with a short-term rental explicitly permitted by the Fannie Mae Second Home Rider. And indeed the second half of 2020, during the height of Covid, was a time when many people were making ad hoc living arrangements. We simply don’t know what happened here. But Lindsey Halligan does know, and she chose not to mention it in this indictment.

In any event, James has not disclosed any income from the Norfolk property, rental or otherwise, since 2020.

The “Crimes”

Suppose for the sake of argument, that James was prohibited from renting the Norfolk property and did so anyway.

The bank fraud statute, 18 U.S.C. § 1344, makes it a crime to “knowingly execute” a “scheme or artifice” to either defraud a bank or, more broadly, to obtain funds from the bank “by means of false or fraudulent pretenses, representations, or promises.” And 18 U.S.C. § 1014 similarly makes it a crime to “knowingly make[] any false statement or report… for the purpose of influencing in any way” a covered mortgage lender.

To convict James, the government must not only prove that she lied on the mortgage application, but that she did so “knowingly” and as part of a corrupt “scheme” to improperly influence the mortgage lender. Prosecutors would have to show that James knew she was going to rent out the Norfolk property at the time she signed the loan application but covered up that fact and that she did so for the purpose of defrauding the bank into offering her a lower rate of interest on the loan.

In other words, if this case were to somehow go to trial, prosecutors would have to prove beyond a reasonable doubt that James concocted a fraudulent scheme in advance to get an eight-tenths-of-one-percent reduction on a modest loan that she voluntarily paid off eleven years early … all so that she could earn a couple thousand dollars in rental income.

When you say it out loud, it doesn’t make much sense. And it’ll probably make even less sense when James herself starts talking.

Thanks for this detailed analysis.

I would just like to add one observation... that when it comes to President Trump's actities as a litigant, it is important for us to remember that he views the law not as a neutral vehicle to obtain redress when wronged, but as a cudgel with which to smite anyone he feels may have wronged or slighted him.

The intent here *may* at least in part be an attempt at whataboutism - an attempt to misdirect his Base by claiming that it is in fact James who is guilty and who has wrongly accused Trump of the very crimes she has been committing. Hmm. I wonder where he might have gotten an idea like that?

But more than this, I think he does it to inflict suffering. He knows that with the full force of the DOJ being brought to bear, he can push this case long and hard, and drag up every last tiny little bit of dirt or theory that he can possibly throw at the wall. Chances are that none of it will stick, of course.

But that's not why he does it. He does it because he knows that James is going to have to pay her legal team to investigate and refute every last item, every last claim in the case. If that's the strategy, it honestly doesn't matter to the President if James is acquitted at the end of the trial. He just wants a nice long trial. A nice, long trial where he can pick up on the "brilliant" job his prosecution Team - sorry, the DOJ - are doing, with daily sniping at James.

she committed mortgage fraud and she said her father was her husband and not to mention she obtained a mortgage by lying about the house in NY being a four family instead of a 5 knowing that was fraud.